The future amount can be a single payment at the date of maturity, a series of payments over future time periods, or a combination of both. The short term notes payable are classified as short-term obligations of a company because their principle amount and any interest thereon is mostly repayable within one year period. They are usually issued for purchasing merchandise inventory, raw materials and/or obtaining short-term loans from banks or other financial institutions. The short-term notes may be negotiable which means that they may be transferred in favor of a third party as a mode of payment or for the settlement of a debt. The short-term notes are reported as current liabilities and their presence in balance sheet impacts the liquidity position of the business. The date of receiving the money is the date that the company commits to the legal obligation that it has to fulfill in the future.

Similarities Between Accounts Payable and Notes Payable

A software company hires a marketing agency on a six-month contract, agreeing to pay the agency $30,000 at the end of the contract period. At the end of the contract, the software company is obligated to pay the marketing agency. This would be classified as accounts payable, a financial obligation from services rendered on credit.

How to Find Notes Payable on a Balance Sheet

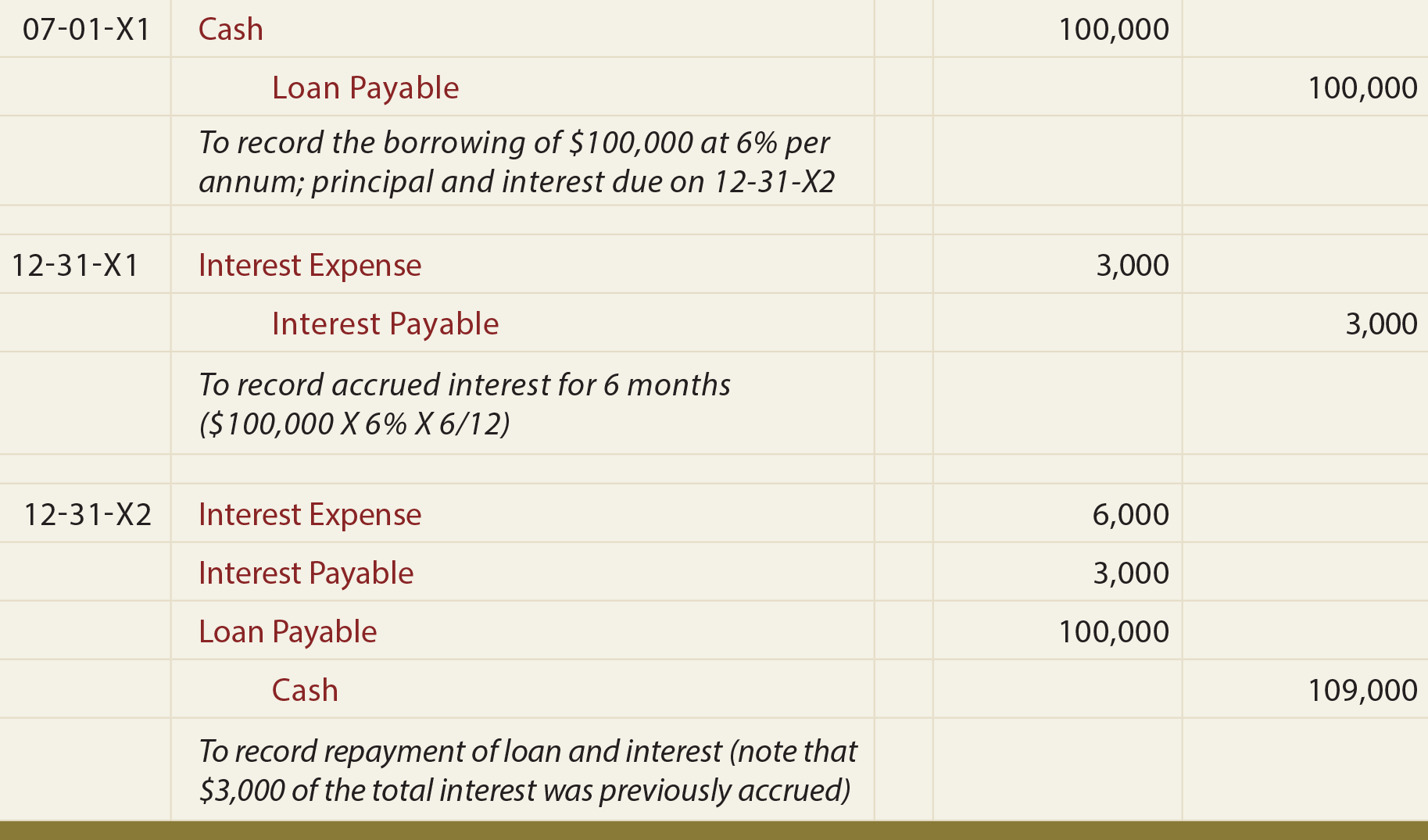

The interest-only type requires borrowers to pay only the applicable interest every month with an assurance of the repayment of the entire principal amount at the end of the loan tenure. Negative agreements require borrowers to pay interest less than the applicable interest charges, thereby adding the remaining amount to the principal balance. Though choosing this option helps people refrain from paying more as interest when inconvenient, the same adds up to the total amount to be repaid in the long run, increasing the burden. National Company prepares its financial statements on December 31 each year. Therefore, it must record the following adjusting entry on December 31, 2018 to recognize interest expense for 2 months (i.e., for November and December, 2018). National Company must record the following journal entry at the time of obtaining loan and issuing note on November 1, 2018.

Top 10 Proven Tips For Automating Your Cash Application Process

These agreements often come with varying timeframes, such as less than 12 months or five years. Notes payable payment periods can be classified into short-term and long-term. Long-term notes payable come to maturity longer than one year but usually within five years or less. Many people argue that if account payable is a short-term liability, why can’t the notes payable for less than one year be treated as account payable. It should be understood that a promissory note or note payable is a legal contract and formal agreement between the borrower and lender. Similarly, when a business entity takes a loan from the bank, purchases bulk inventory from a supplier, or acquires equipment on credit, notes payables are often signed between the parties.

How to find notes payable on a balance sheet

When you repay the loan, you’ll debit your Notes Payable account and credit your Cash account. For the interest that accrues, you’ll also need to record the amount in your Interest Expense and Interest Payable accounts. Kelly shortlists a residential property and decides to go ahead with it. She contacts a lending institution, and they agree to pay the required amount. The latter prepares the notes payable with all the details to sign and get it signed by themselves and Kelly, respectively.

Journal entries for zero-interest-bearing note:

- A small manufacturing company needs additional funds to expand its operations.

- These examples show the practical application of accounts payable and notes payable in everyday business scenarios.

- A note payable is an unconditional written promise to pay a specific sum of money to the creditor, on demand or on a defined future date.

This blog will help you understand what notes payables are, who signs the notes, examples, and accounting treatment for the company’s notes payable. To summarize, the present value (discounted cash flow) of $4,208.40 is the fair value of the $5,000 note at the time of the purchase. The additional amount received of $791.60 ($5,000.00 – $4,208.40) is the interest component paid to the creditor over the life of the two-year note.

The agreement calls for Ng to make 3 equal annual payments of $6,245 at the end of the next 3 years, for a total payment of $18,935. If neither of these amounts can be determined, the note should be recorded at its present value, using an appropriate interest rate for that type of note. This situation may occur when a seller, in order to make a detail appear more favorable, increases the list or cash price of an item but offers the buyer interest-free repayment terms.

At the same time, notes payment is a credit entry as they promise repayment, which is a liability. Notes Payable are a promise in writing whereby a borrower assures repaying the lenders within a specific period. These promissory notes indicate the loan that one party lends to the other, expecting the timely repayment, which may be the principal alone or the principal along with the interest amount.

The company usually issue notes payable to meet short-term financing needs. As the company pays off the loan, the amount under “notes payable” in its liability account will decrease. At the same time, the amount recorded for “furniture” under the asset account will also see some decrease by way of accounting for the depreciation of the asset (furniture) over time. Notes payable is a liability that arises when a business borrows money and signs a written agreement with a lender to pay back the borrowed amount of money with interest at a certain date in the future. However, the notes payable are written on the will of both parties.

On the other hand, short-term agreements are treated as current liabilities. Finally, at the end of the 3 month term the notes payable have to be paid together with the accrued interest, and the following journal completes the transaction. Taking out a loan directly from the bank can be done relatively easily, but there are is notes payable an asset fees for this (and interest rates). Issuing notes payable is not as easy, but it does give the organization some flexibility. For example, if the borrower needs more money than originally intended, they can issue multiple notes payable. The adjusting journal entry in Case 1 is similar to the entries to accrue interest.

For instance, a bank loan to be paid back in 3 years can be recorded by issuing a note payable. The nature of note payable as long-term or short-term liability entirely depends on the terms of payment. A note payable is an unconditional written promise to pay a specific sum of money to the creditor, on demand or on a defined future date. These notes are negotiable instruments in the same way as cheques and bank drafts. The lender may require restrictive covenants as part of the note payable agreement, such as not paying dividends to investors while any part of the loan is still unpaid. If a covenant is breached, the lender has the right to call the loan, though it may waive the breach and continue to accept periodic debt payments from the borrower.